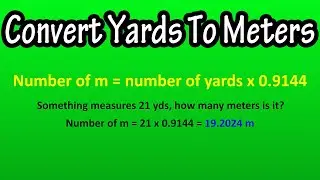

The Specific Identification Method To Value Inventory Explained - Calculate Cost Of Goods Sold

In this video we discuss the specific identification method to value inventory. We cover the 3 steps of this method including how to calculate the cost of goods sold

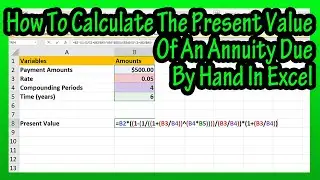

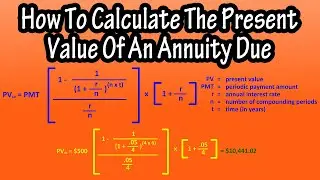

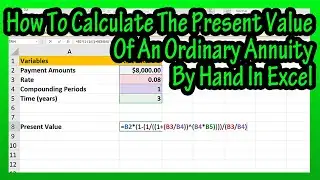

Transcript/notes

The specific identification method to value inventory is often used when a business can rather easily identify the original purchase cost of an item with the item.

To calculate inventory value using this method, there are 3 steps. Calculate the cost of goods, or merchandise available for sale, calculate the cost of the ending inventory and calculate the cost of goods sold, which is actually step 1 minus step 2.

Let’s go through a very basic example of this to value inventory. A business sells a particular item, and color codes the boxes as they come into the store, this way they can easily attach a specific invoice cost to each item.

The beginning inventory had 25 items at a cost of $12 per unit, which has a total cost of $300. There first purchase of the item was on March 1st, for 15 units at a cost of $15 per unit for a total cost of $225. Then they made the following purchases of units at the beginning of June, September, and November. And I have listed the cost per units and the total costs in this table.

If we sum up the number of units purchased, we get 95, and if we sum up the total cost column, we have $1540. This total is the goods or merchandise or cost of goods available for sale. Which is the 1st step.

During this time period, the business sold 70 units of the 95 units purchased, so 95 minus 70, or 25 units are in the ending inventory.

Now, the business counts the number of color coded units left in the ending inventory. They find that they have 10 units from the March 1st purchase at a cost of $15 per unit, 10 units from the September purchase at $18 per unit, and 5 units from the November purchase at $20 per unit. And here are the total costs for these units from their purchase dates, which is $430. And this $430 is the cost of the ending inventory, which is the 2nd step.

And now we can do the 3rd step, calculate the cost of goods sold. The formula is cost of goods sold equals the cost of goods available for sale minus the cost of ending inventory. So, we have $1540, minus $430, which equals $1110 as the cost of goods sold. And that completes the process.

Chapters/Timestamps

0:00 What is the specific identification method to value inventory

0:10 The 3 steps of specific identification

0:25 Example using the specific identification method to value inventory

0:41 S1 - How to calculate the cost of goods available for sale

1:20 S2 - How to calculate the cost of ending inventory

2:01 S3 - How to calculate the cost of goods sold

![Best Dubstep Mix 2021 [Brutal Dubstep Drops],Gaming Dubstep Mix](https://images.videosashka.com/watch/hskp_5uxw00)

![Everyone Bullies Ui-mama With Ui-Beams (Koyori, Lize, Furen, Haneru, Patra, Siro, Aoi) [Eng Subs]](https://images.videosashka.com/watch/2kYfGFujdVs)