Credit Risk - Probability of Default, End-to-End Model Development | Beginner to Pro Level

Credit Risk Modelling | End - to - End Development of Probability of Default Credit Risk| Kaggle Competition Data

Banks play a crucial role in market economies. They decide who can get finance and on what terms and can make or break investment decisions. For markets and society to function, individuals and companies need access to credit.

Credit scoring algorithms, which make a guess at the probability of default, are the method banks use to determine whether or not a loan should be granted.

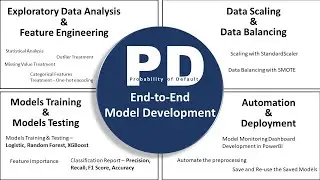

In this video we have started such development of PD model, absolutely from a beginner level and have explored the data widely to come up with a conclusive data which fits best for the model and have developed the model using XGBoost.

It is expected that you have some basic understanding of Python and Banking domain and after watching this video you would be in very good position to pick any given data and start with your own development.

You might also like to watch -

Exploratory Data Analysis - • EDA - Exploratory Data Analysis | EDA...

Credit Card Fraud Detection ML Model - • Data Science | Credit Card Fraud Dete...

Logistic Regression Model Development - • Mastering Logistic Regression in Pyth...

Linear Regression Model Development - • Data Science | How to Make Linear Reg...

Decision Tree Model Development - • Machine Learning Project: Decision Tr...

Data Science Full Playlist - • Data Science

URL for Kaggle competition discussed in the video - https://www.kaggle.com/c/GiveMeSomeCr...

To Download the script created in the video -

File Name - PD_credit_risk_model_dev.py

URL - https://github.com/LEARNEREA/Data_Sci...

credit risk,

credit risk modelling,

credit risk analysis,

Banking, XGBoost

IFRS9, Basel

#CreditRisk #ProbabilityOfDefault #Banking #MachineLearning #PythonProgramming #XGBoost