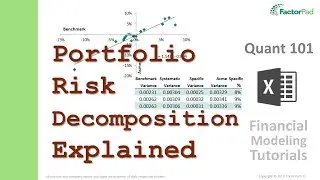

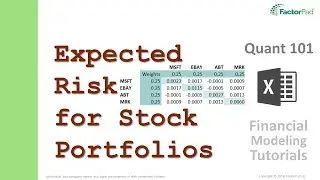

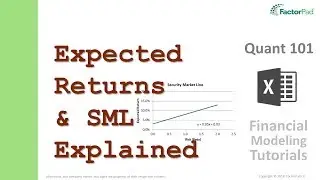

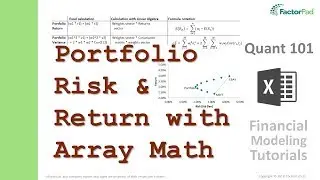

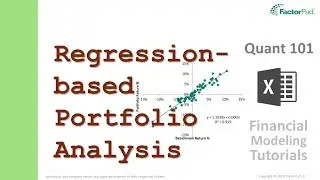

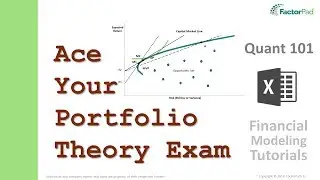

Stock portfolio risk decomposition into systematic risk and specific risk

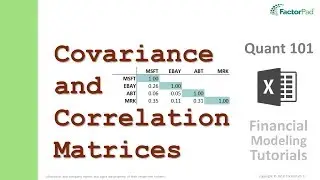

A financial modeling tutorial on finding systematic risk and specific risk by decomposing risk on a stock portfolio as done in financial risk management software with other terms unsystematic risk, diversifiable risk, non-diversifiable risk, idiosyncratic risk and residual risk often used.

For the full video transcript and key Excel formulas see:

https://factorpad.com/fin/quant-101/p...

Zoom straight to the section you are interested in here:

00:37 - Video Outline

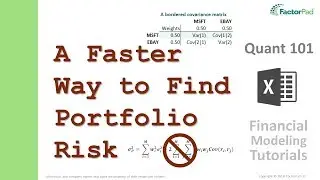

01:04 - Step 1 - Create an Active Portfolio

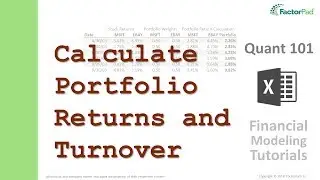

03:52 - Step 2 - Pull Forward Returns

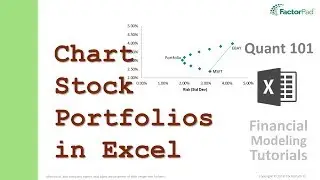

04:46 - Step 3 - Create a Scatter Plot

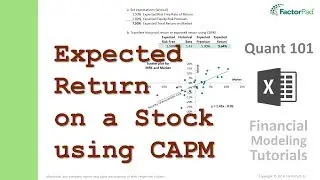

06:36 - Step 4 - Analyze the Return and Risk Decomposition

15:44 - Summary

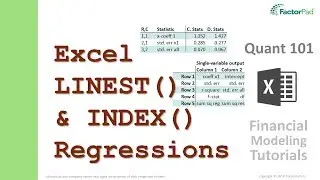

16:14 - Step 5 - Next: Excel's Data Analysis Regression

For the Outline to the Quant 101 series see:

https://factorpad.com/fin/quant-101/q...

See other portfolio and statistics related content here:

https://factorpad.com

Happy Learning!